Power Grid Expansion Forecast 2026-2040

SOLARTODO Editorial Team

Solar Energy & Infrastructure Expert Team

Watch the video

TL;DR

From 2026 to 2040, tower demand will grow fastest in 10kV-35kV networks by unit volume and in 110kV-220kV corridors by project value. According to IEA, grid investment must climb from about $390 billion in 2024 to roughly $600 billion by 2030, while more than 80 million km of grids need expansion or refurbishment by 2040. For urban projects, compact monopoles offer the strongest ROI through smaller footprints and faster erection.

Global grid investment must rise from about $390 billion in 2024 to roughly $600 billion per year by 2030, while transmission line additions need to exceed 80 million km by 2040; demand will concentrate in 10kV, 110kV, and 220kV tower and monopole classes.

Summary

Global grid investment must rise from about $390 billion in 2024 to roughly $600 billion per year by 2030, while transmission line additions need to exceed 80 million km by 2040; demand will concentrate in 10kV, 110kV, and 220kV tower and monopole classes.

Key Takeaways

- Prioritize 110kV and 220kV procurement because these classes will carry a large share of urban-suburban expansion from 2026-2040, with corridor pressure rising as electricity demand grows more than 3% annually in many emerging markets.

- Standardize 10kV distribution poles at 18m class heights and 100m design spans for municipal feeder projects where compact footprints can reduce occupied land by 50-70% versus comparable lattice structures.

- Use 35m 110kV octagonal monopoles for city-entry and suburban transmission where 250m design spans and 20-40% faster erection can improve EPC schedules and reduce traffic disruption.

- Select 40m 220kV dodecagonal monopoles for double-circuit corridors requiring 300m design spans, ACSR-400 conductor compatibility, and 40-60% lower footprint than conventional lattice alternatives.

- Model EPC budgets with three tiers—FOB Supply, CIF Delivered, and EPC Turnkey—and apply volume discounts of 5% at 50+ units, 10% at 100+, and 15% at 250+ units.

- Verify design compliance with IEC 60826, ASCE 10-15, IEEE 738, and project-specific galvanization requirements of 70-100 micrometers to support 50-year design life targets.

- Plan payback on compact steel monopoles through lower right-of-way, faster erection, and reduced civil complexity; urban projects often recover premium capital in 4-8 years through land and schedule savings.

- Engage bankable suppliers such as SOLAR TODO early for 2026-2030 framework contracts because long-cycle steel, zinc, and logistics constraints can extend tower delivery lead times by 12-24 weeks.

Global Grid Expansion Outlook 2026-2040

According to IEA (2024), annual grid investment must increase from about $390 billion in 2024 to nearly $600 billion by 2030, making transmission and distribution hardware one of the fastest-growing infrastructure categories through 2040.

The core procurement question for utilities, EPC firms, and industrial developers is not whether grid expansion will happen, but which voltage classes will absorb the highest capital and steel tonnage. According to the International Energy Agency, electricity demand growth from electrification, cooling, data centers, EV charging, and renewable integration is forcing both transmission reinforcement and medium-voltage distribution densification. The International Energy Agency states, "Grids are the backbone of electricity systems," and delayed network build-out is now a primary bottleneck for clean energy deployment.

From a tower demand perspective, the market is bifurcating. Lower-voltage 10kV to 35kV structures will dominate by unit count because distribution networks require denser pole spacing, while 110kV to 220kV structures will dominate by steel weight, engineering complexity, and project value. According to IRENA (2024), global renewable power capacity reached 3,870 GW in 2023, up nearly 14% year over year, and every incremental gigawatt of variable renewable generation increases pressure on grid interconnection corridors.

For B2B buyers, the implication is clear: framework sourcing must align tower class with network function. Municipal utilities may procure hundreds of 10kV and 35kV poles for feeder modernization, while national utilities and IPP interconnection projects will increasingly specify 110kV and 220kV monopoles where right-of-way is constrained.

Grid investment trend, 2022-2040

According to BloombergNEF (2024), global energy transition investment reached about $1.77 trillion in 2023, yet grid spending remains below the level needed to support electrification and renewable integration at scale. Wood Mackenzie (2024) similarly notes that transmission queues and permitting delays are extending project timelines in North America, Europe, and parts of Asia.

| Year/Period | Global Grid Investment Estimate | Key Market Signal | Tower Demand Implication |

|---|---|---|---|

| 2022 | ~$330 billion | Post-pandemic grid capex recovery | Replacement and delayed upgrades |

| 2024 | ~$390 billion | Renewable interconnection bottlenecks intensify | Higher demand for 10kV-220kV structures |

| 2030 | ~$600 billion/year target | IEA-aligned acceleration case | Large-scale framework procurement |

| 2040 | Sustained elevated spending | Electrified transport and industry | Long-cycle transmission expansion |

Regional demand by network layer

According to IEA (2023), more than 80 million km of grids need to be added or refurbished by 2040 to meet national climate and energy goals. That figure includes both transmission and distribution assets, but distribution accounts for most route length, while transmission accounts for a disproportionate share of project capital.

| Region | 2026-2030 Primary Need | 2031-2040 Primary Need | High-Demand Voltage Classes |

|---|---|---|---|

| Asia-Pacific | Urban distribution growth, renewable evacuation | UHV and suburban reinforcement | 10kV, 35kV, 110kV, 220kV |

| Europe | Grid refurbishment, offshore landing corridors | Cross-border reinforcement | 35kV, 110kV, 220kV |

| North America | Interconnection backlog relief, wildfire hardening | Long-distance transmission | 35kV, 110kV, 220kV |

| Middle East & Africa | New electrification and industrial grids | Utility-scale solar and mining corridors | 10kV, 35kV, 110kV |

| Latin America | Distribution densification, renewable integration | Regional transmission strengthening | 10kV, 35kV, 110kV, 220kV |

Tower Demand by Voltage Class

Tower demand from 2026-2040 will be highest by unit count in 10kV-35kV networks and highest by project value in 110kV-220kV corridors, with urban monopoles gaining share because they can cut footprint by 40-75%.

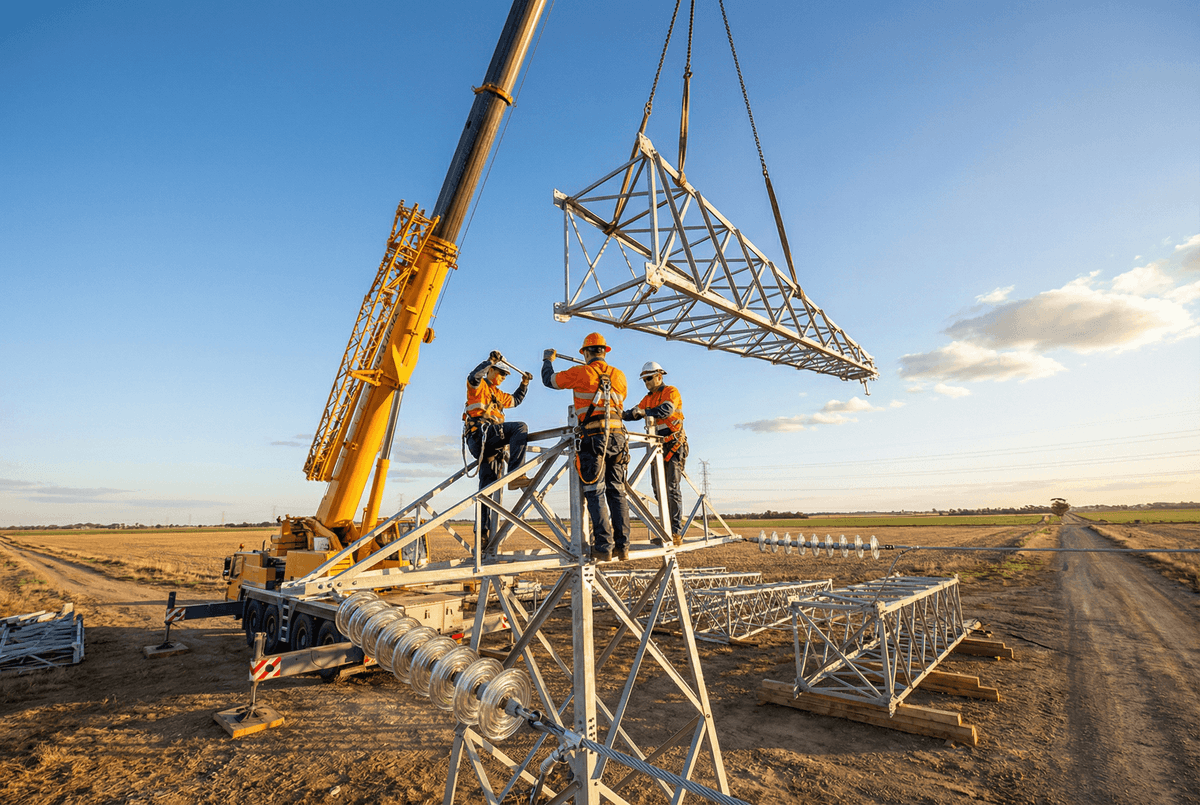

Voltage class determines not only mechanical loading, but also procurement logic, foundation design, transport strategy, erection sequence, and permitting risk. For buyers comparing lattice versus monopole options, the key variables are span length, conductor configuration, right-of-way width, urban aesthetics, and installation speed.

10kV class: distribution volume leader

The 10kV segment will remain the largest by pole count because it supports municipal feeders, industrial parks, campuses, and peri-urban electrification. A typical 18m 10kV tapered monopole with slip-joint connection supports around 100m design spans and double-circuit distribution duty. Compared with conventional lattice alternatives, this format can reduce footprint by 50-70% and visible structural complexity by more than 30% in dense streetscapes.

This matters in Latin America, Southeast Asia, and Africa, where city expansion often requires rapid feeder extension with minimal land acquisition. For procurement teams, 10kV projects are usually less steel-intensive per unit but more sensitive to batch standardization, galvanization quality, and logistics efficiency across hundreds of sites.

35kV to 110kV class: suburban and industrial backbone

The 35kV and 110kV range is the transition layer between distribution and transmission. According to S&P Global Commodity Insights (2024), industrial electrification, data center growth, and renewable interconnection are increasing sub-transmission build-out in manufacturing belts and suburban load centers.

A 35m 110kV octagonal transmission pole with flanged sections and a 250m design span is well suited to urban-suburban corridors. This class can reduce occupied ground area by about 60-75% compared with conventional lattice towers and shorten erection activities by 20-40%, especially where sectional transport and crane access are manageable.

220kV class: high-value growth segment

The 220kV segment will see strong growth where utilities need double-circuit capacity without wide right-of-way acquisition. A 40m 220kV dodecagonal transmission pole typically supports 300m design spans, two circuits, and ACSR-400 conductors, while reducing footprint by about 40-60% versus angle-steel lattice structures.

This class is especially relevant in mixed residential-industrial zones and suburban transmission corridors. According to IEA (2024), grid congestion is increasingly concentrated near load centers and renewable hubs, which makes compact, faster-to-permit steel monopoles attractive despite higher unit prices.

| Voltage Class | Typical Application | Typical Height | Typical Span | Main Demand Driver 2026-2040 |

|---|---|---|---|---|

| 10kV | Urban distribution feeders | 18m | 80-120m | Electrification and feeder densification |

| 35kV | Industrial and sub-transmission | 20-30m | 120-180m | Industrial parks and utility upgrades |

| 110kV | City-entry transmission | 35m | 200-250m | Renewable interconnection, urban reinforcement |

| 220kV | Regional/suburban transmission | 40m | 250-300m | Capacity expansion and double-circuit corridors |

Technical Design Trends and Procurement Criteria

From 2026 onward, buyers will favor standardized galvanized steel monopoles with 50-year design life, 70-100 micrometer zinc coating, and compliance with IEC 60826, IEEE 738, and ASCE 10-15 methodologies.

The technical shift is driven by three realities. First, urban and suburban corridors are land-constrained. Second, utilities need predictable erection schedules. Third, project financiers increasingly prefer standardized, bankable designs with traceable materials and codified load assumptions.

According to IEC 60826, overhead line design must account for climatic loads, reliability levels, and broken-wire contingencies. According to IEEE 738, conductor temperature and current relationships directly affect ampacity assumptions, which in turn influence tower loading and clearance design. For EPC teams, this means tower selection cannot be separated from conductor choice, wind zone, ice loading, and fault contingency criteria.

Monopole versus lattice selection logic

Monopoles are not universally superior, but they are increasingly preferred in city and suburban projects. Their advantages include smaller footprints, lower visual clutter, and simpler corridor permitting. Their trade-offs include higher shaft fabrication precision, larger foundation concentration at a single point, and crane-dependent erection.

Lattice towers remain competitive in remote corridors, heavy angle applications, and very high mechanical load conditions. However, where land cost is high or permitting is politically sensitive, monopoles often deliver lower total project cost even when unit steel pricing is higher.

| Structure Type | Footprint Reduction vs Lattice | Erection Speed | Best Use Case | Buyer Trade-Off |

|---|---|---|---|---|

| Tapered monopole | 50-70% | Fast | 10kV urban distribution | Precision fabrication needed |

| Octagonal monopole | 60-75% | Fast to medium | 110kV city-entry corridors | Flange alignment and crane planning |

| Dodecagonal monopole | 40-60% | Medium | 220kV suburban double-circuit | Higher unit cost, stronger foundations |

| Conventional lattice | Baseline | Medium to slow | Remote, low-land-cost routes | Larger ROW and visual impact |

The Fraunhofer ISE perspective on energy infrastructure is relevant here: system value increasingly depends on integration efficiency, not only generation cost. Fraunhofer ISE (2024) states that grid expansion and flexibility are essential to convert low-cost renewable electricity into usable delivered power. For tower buyers, that translates into prioritizing designs that shorten permitting and construction time.

Regional Forecast and Year-over-Year Trend Analysis

Asia-Pacific will lead tower demand through 2040, while Europe and North America will spend more per route-kilometer on compact, higher-specification structures for constrained corridors and grid modernization.

Historical and forecast analysis shows a clear sequencing pattern. Between 2021 and 2024, utilities focused on delayed upgrades, renewable interconnections, and replacement of aging assets. In 2025-2026, procurement is shifting toward framework agreements and standardized tower families. From 2027 to 2030, the market should accelerate as transmission bottlenecks become a direct constraint on industrial growth and decarbonization. From 2030 to 2040, digitalized grid planning, higher conductor temperatures, and hybrid AC corridor upgrades will reshape tower specifications.

2021-2026 historical to current trend

According to IRENA (2024), renewable additions have continued to outpace grid reinforcement in many markets, creating interconnection queues and curtailment risk. According to NREL (2024), transmission expansion remains one of the highest-leverage enablers for lowering system-wide electricity costs in high-renewable grids.

2027-2030 near-term forecast

The near-term market will favor 110kV and 220kV structures around renewable hubs, industrial zones, and city perimeters. Steel price volatility and zinc coating costs will remain procurement risks, but standardized families can reduce engineering hours by 10-20% and improve tender comparability.

2030-2040 long-term outlook

By the 2030s, tower demand will increasingly reflect climate resilience requirements, including higher wind loading, corrosion resistance, and wildfire-related line hardening in selected regions. Digital inspection, drone-based condition monitoring, and line uprating will also increase retrofit demand, not only greenfield demand.

| Region | 2025-2026 Status | 2027-2030 Outlook | 2030-2040 Scenario |

|---|---|---|---|

| Asia-Pacific | Fast urban and industrial expansion | Strong 110kV/220kV growth | Large-scale corridor reinforcement |

| Europe | Aging asset replacement | Cross-border and offshore links | Dense compact transmission upgrades |

| North America | Queue relief and resilience spending | Long-distance transmission acceleration | Hardening and reconductoring growth |

| Middle East & Africa | New-build electrification | Solar-driven substation and feeder growth | Mining, desalination, and industrial grids |

| Latin America | Distribution densification | Renewable evacuation corridors | Regional interconnection strengthening |

EPC Investment Analysis and Pricing Structure

EPC buyers should evaluate tower projects using FOB Supply, CIF Delivered, and EPC Turnkey pricing because logistics, foundations, and erection can add 25-80% above ex-works steel cost depending on voltage class and site conditions.

For B2B procurement, tower pricing is never just a steel question. Engineering scope, geotechnical risk, transport access, galvanization specification, foundation volume, and erection method all affect total installed cost. SOLAR TODO typically supports inquiry-led quotation rather than online checkout, which is appropriate for utility and EPC projects requiring load verification and project-specific compliance.

What EPC turnkey delivery includes

A turnkey package generally includes:

- Structural design verification and shop drawings

- Steel shaft or lattice fabrication

- Hot-dip galvanization and QA documentation

- Anchor bolts, templates, and embedded parts

- Logistics coordination and packing lists

- Foundation design support

- Erection supervision or full installation

- As-built documentation and punch-list closeout

Three-tier pricing model

| Pricing Tier | What Is Included | Typical Buyer Use |

|---|---|---|

| FOB Supply | Tower steel, bolts, drawings, factory QA | Buyers with local freight and installation teams |

| CIF Delivered | FOB plus sea freight and insurance | Importers needing landed-cost certainty |

| EPC Turnkey | CIF plus civil works, erection, testing | Utilities and developers seeking single-point delivery |

Indicative commercial logic by class is straightforward: 10kV poles are usually the lowest unit-cost but highest volume; 110kV monopoles carry higher fabrication and flange costs; 220kV double-circuit poles carry the highest steel tonnage, foundation demand, and erection complexity. Volume pricing guidance should be built into framework contracts: 50+ units can target a 5% discount, 100+ units 10%, and 250+ units 15%, subject to steel index movement and delivery schedule.

ROI and payback logic

Urban monopoles often justify higher capex through lower land occupation, shorter outages, and faster permit approval. In dense corridors, total project savings from reduced right-of-way, fewer traffic interventions, and shorter erection windows can offset the monopole premium in roughly 4-8 years. Distribution-class 10kV replacements often show the fastest operational payback, while 110kV and 220kV projects deliver stronger strategic ROI through congestion relief and new load connection capacity.

Payment terms and financing

Standard export terms commonly include 30% T/T in advance and 70% against B/L, or 100% L/C at sight. Financing may be available for large projects above $1,000K, particularly where utility off-take or sovereign-backed infrastructure programs support bankability. For project quotations, buyers can contact SOLAR TODO at [email protected] or call +6585559114.

Supplier Selection and Product Fit for 10kV, 110kV, and 220kV Projects

Selecting the correct tower family requires matching voltage, span, circuit count, and corridor constraints because a 10kV 18m feeder pole, a 35m 110kV monopole, and a 40m 220kV double-circuit pole solve fundamentally different grid problems.

SOLAR TODO’s current power tower portfolio aligns well with the forecast demand pattern. The 18m 10kV tapered monopole urban aesthetic slip-joint model fits municipal and industrial feeder upgrades where compact land occupation and standardized erection matter. The 35m 110kV octagonal transmission pole flanged model suits city transmission and suburban corridors requiring a 250m design span and a cleaner skyline. The 40m 220kV dodecagonal transmission pole addresses higher-capacity suburban transmission with double-circuit duty and 300m design spans.

For procurement managers, a practical selection framework includes:

- Use 10kV tapered monopoles for dense urban distribution and campus grids

- Use 110kV octagonal monopoles for city-entry, industrial, and suburban transmission

- Use 220kV dodecagonal monopoles where double-circuit capacity and corridor compression are critical

- Verify local wind, ice, seismic, and corrosion assumptions before finalizing steel tonnage

- Lock galvanization, bolt grade, and coating inspection criteria into the tender package

The bottom-line sourcing strategy is to standardize where possible and customize only where loading or permitting requires it. That approach reduces engineering cycle time, improves spare-part compatibility, and supports multi-year capex planning.

FAQ

Q: What voltage class will generate the most tower demand between 2026 and 2040? A: By unit count, 10kV and 35kV classes will generate the most demand because distribution networks require dense pole spacing. By project value and steel tonnage, 110kV and 220kV will be the strongest segments because they support renewable interconnection, urban reinforcement, and double-circuit capacity expansion.

Q: Why are monopoles gaining market share over lattice towers? A: Monopoles are gaining share because they can reduce footprint by roughly 40-75% and often shorten erection time by 20-40% in constrained corridors. They are especially attractive in urban and suburban projects where land cost, aesthetics, and permitting speed matter more than minimum first-cost steel pricing.

Q: What is the best use case for an 18m 10kV tapered monopole? A: An 18m 10kV tapered monopole is best for municipal feeders, industrial parks, campuses, and peri-urban distribution upgrades. With typical 100m design spans and compact foundations, it supports rapid deployment where right-of-way is tight and visual impact must be minimized.

Q: When should buyers choose a 35m 110kV octagonal transmission pole? A: Buyers should choose a 35m 110kV octagonal pole for city-entry and suburban transmission lines needing around 250m design spans and single-circuit duty. It is a strong option when compact footprint, sectional transport, and faster erection are more important than the lowest possible material cost.

Q: What makes a 40m 220kV dodecagonal pole suitable for high-capacity corridors? A: A 40m 220kV dodecagonal pole is suitable because it supports double-circuit configurations, about 300m design spans, and ACSR-400 conductor classes. It also offers stronger torsional performance than many lower-sided shafts, which helps in unbalanced load and broken-wire scenarios.

Q: How should EPC contractors compare FOB, CIF, and turnkey pricing? A: FOB Supply covers fabricated steel and factory scope only, CIF adds freight and insurance, and EPC Turnkey includes civil works, erection, and commissioning support. For realistic budgeting, contractors should assume logistics and installation can add 25-80% above ex-works cost depending on voltage class and site complexity.

Q: What payment terms are typical for export tower projects? A: Common payment terms are 30% T/T in advance and 70% against B/L, or 100% L/C at sight. For larger utility and infrastructure packages above $1,000K, structured financing may be available if the project has strong credit support and a clear implementation schedule.

Q: How long is the design life of modern galvanized steel monopoles? A: Modern galvanized steel monopoles are commonly designed for 50 years under standard maintenance assumptions. Achieving that life depends on correct steel grade, coating thickness—often 70-100 micrometers—site corrosion classification, and periodic inspection of bolts, base plates, and protective systems.

Q: Which standards should buyers request in tower tenders? A: Buyers should typically request design alignment with IEC 60826, IEEE 738, and ASCE 10-15, plus project-specific material and galvanization standards. Tender documents should also define wind, ice, seismic, conductor, broken-wire, and deflection criteria so suppliers can provide comparable structural calculations.

Q: How can buyers reduce procurement risk for 2026-2030 projects? A: Buyers can reduce risk by standardizing tower families, locking steel and zinc adjustment formulas, and prequalifying suppliers 6-12 months before construction. Early framework agreements also help secure factory slots, stabilize lead times, and improve consistency across multi-site utility programs.

References

- International Energy Agency (2024): World Energy Investment 2024; notes grid investment around $390 billion in 2024 and the need for substantial acceleration.

- International Energy Agency (2023): Electricity Grids and Secure Energy Transitions; states more than 80 million km of grids must be added or refurbished by 2040.

- International Renewable Energy Agency (2024): Renewable Capacity Statistics 2024; reports global renewable power capacity of 3,870 GW in 2023.

- BloombergNEF (2024): Energy Transition Investment Trends 2024; tracks global energy transition investment at about $1.77 trillion in 2023.

- Wood Mackenzie (2024): Power and Renewables market analysis; highlights transmission bottlenecks, interconnection queues, and grid modernization demand.

- IEC 60826 (2017): Design criteria of overhead transmission lines; defines loading and reliability methodology for line design.

- IEEE 738 (2023): Standard for calculating the current-temperature relationship of bare overhead conductors.

- ASCE 10-15 (2015): Design of Latticed Steel Transmission Structures; widely used structural design basis for overhead line assets.

Conclusion

Power grid expansion from 2026 to 2040 will be driven by distribution volume in 10kV-35kV networks and capital-intensive growth in 110kV-220kV corridors, with compact monopoles cutting footprint by 40-75% and supporting faster urban deployment.

For utilities and EPC buyers, the best strategy is to lock in standardized tower families now, align tenders with IEC 60826 and IEEE 738, and source through qualified partners such as SOLAR TODO before grid investment rises toward $600 billion per year by 2030.

About SOLARTODO

SOLARTODO is a global integrated solution provider specializing in solar power generation systems, energy-storage products, smart street-lighting and solar street-lighting, intelligent security & IoT linkage systems, power transmission towers, telecom communication towers, and smart-agriculture solutions for worldwide B2B customers.

Further Reading

About the Author

SOLARTODO Editorial Team

Solar Energy & Infrastructure Expert Team

SOLAR TODO is a professional supplier of solar energy, energy storage, smart lighting, smart agriculture, security systems, communication towers, and power tower equipment.

Our technical team has over 15 years of experience in renewable energy and infrastructure, providing high-quality products and solutions to B2B customers worldwide.

Expertise: PV system design, energy storage optimization, smart lighting integration, smart agriculture monitoring, security system integration, communication and power tower supply.

Cite This Article

SOLARTODO Editorial Team. (2026). Power Grid Expansion Forecast 2026-2040. SOLARTODO. Retrieved from https://solartodo.com/knowledge/power-grid-expansion-forecast-2026-2040-tower-demand-by-voltage-class

@article{solartodo_power_grid_expansion_forecast_2026_2040_tower_demand_by_voltage_class,

title = {Power Grid Expansion Forecast 2026-2040},

author = {SOLARTODO Editorial Team},

journal = {SOLARTODO Knowledge Base},

year = {2026},

url = {https://solartodo.com/knowledge/power-grid-expansion-forecast-2026-2040-tower-demand-by-voltage-class},

note = {Accessed: 2026-07-21}

}Published: July 12, 2026 | Available at: https://solartodo.com/knowledge/power-grid-expansion-forecast-2026-2040-tower-demand-by-voltage-class

Subscribe to Our Newsletter

Get the latest solar energy news and insights delivered to your inbox.

View All Articles