Global Solar PV Market Report 2026

SOLAR TODO

Solar Energy & Infrastructure Expert Team

Watch the video

TL;DR

Global solar PV in 2026 is a scale and cost story: installed capacity is moving above 2.2 TW, utility-scale generation remains near $0.03-$0.05/kWh, and many commercial projects still achieve 4-7 year payback. For B2B buyers, the winning strategy is to combine bankable N-type technology, accurate yield modeling, and clear EPC scope to stay competitive through the 2035 expansion cycle.

Global solar PV capacity is moving from roughly 1.6 TW in 2024 toward more than 2.2 TW by 2026, while utility-scale LCOE remains near $0.029-$0.049/kWh and annual additions could exceed 1 TW before 2030 in accelerated scenarios.

Summary

Global solar PV capacity is moving from roughly 1.6 TW in 2024 toward more than 2.2 TW by 2026, while utility-scale LCOE remains near $0.029-$0.049/kWh and annual additions could exceed 1 TW before 2030 in accelerated scenarios.

Key Takeaways

- Prioritize markets with electricity tariffs above $0.10/kWh, where commercial solar PV often reaches payback in 4-7 years and utility-scale projects can clear sub-$0.05/kWh generation costs.

- Select N-type TOPCon or advanced bifacial modules with 22.5%-24.5% efficiency to improve land productivity by 5%-12% versus older PERC fleets in 2026 procurement cycles.

- Model projects using regional yield bands of 1,200-1,800 kWh/kWp/year, because a 50 kWp system can generate about 75-90 MWh/year in strong commercial irradiation zones.

- Compare fixed-tilt and tracker designs carefully, as single-axis trackers can raise annual generation by 15%-25% and bifacial gain can add another 10%-30% under suitable albedo conditions.

- Lock in EPC scope early, because turnkey delivery typically shifts capex by 10%-20% versus supply-only pricing but reduces interface risk, schedule delays, and performance disputes.

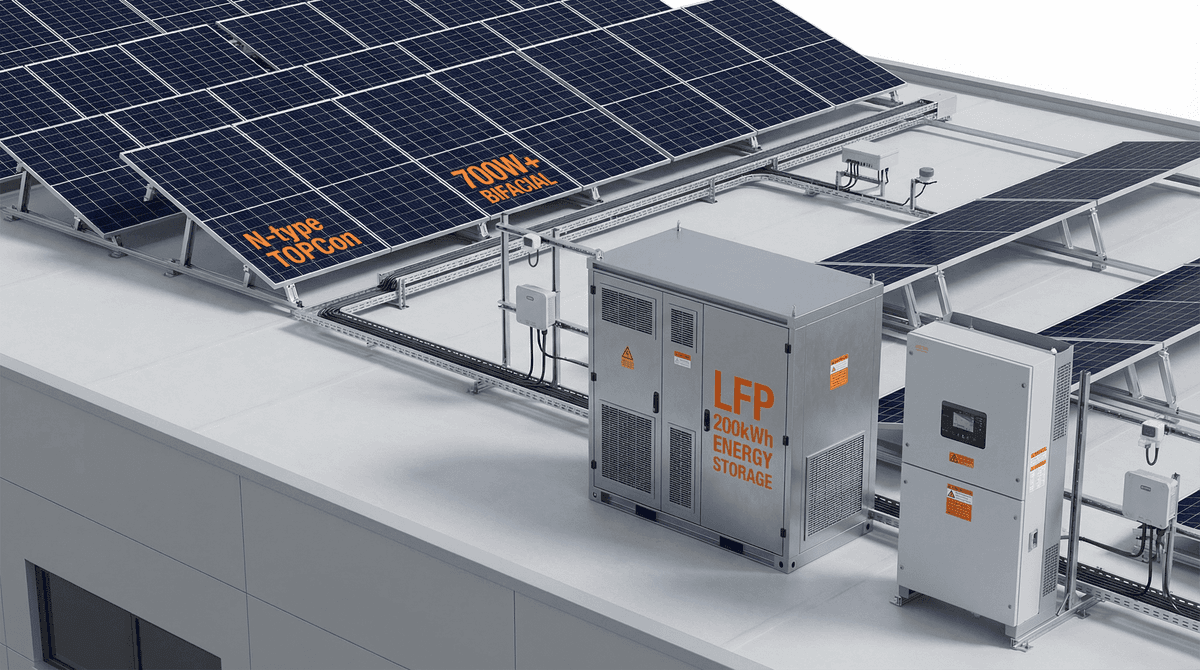

- Use LFP battery coupling where outage resilience or low export tariffs matter, since a 50 kWh battery can support critical loads of 3-8 kW for roughly 6-16 hours.

- Verify IEC 61215, IEC 61730, IEEE 1547, and local grid-code compliance to protect bankability, interconnection approval, and long-term O&M performance over 25-30 years.

- Negotiate volume purchases above 50 units or multi-MW portfolios, where supply discounts of 5%-15% can materially improve IRR and shorten payback by 0.3-1.0 years.

Global Solar PV Market Overview in 2026

Global solar PV is entering a scale phase where installed capacity passes about 2.2 TW by 2026, annual additions approach 600-800 GW, and benchmark utility LCOE stays near $0.03-$0.05/kWh in strong-resource markets.

According to IRENA (2024), global renewable power capacity reached 3,870 GW in 2023, with solar accounting for 1,419 GW and adding 345.5 GW in a single year. According to the IEA (2024), solar PV is set to become the largest renewable source by installed capacity before 2030, supported by manufacturing expansion, lower module prices, and rising electrification demand. For B2B buyers, the key implication is simple: solar is no longer a niche decarbonization tool but a mainstream power procurement asset.

The 2025-2026 market is defined by three structural shifts. First, module oversupply has compressed prices faster than balance-of-system costs, improving project economics but increasing supplier selection risk. Second, N-type TOPCon and bifacial products are replacing older P-type technologies in mainstream tenders. Third, storage pairing is becoming more common as grids tighten export rules and time-of-use price spreads widen.

The International Energy Agency states, "Solar PV has become the cheapest source of electricity in many parts of the world." That statement matters for procurement teams because it reframes solar from sustainability spending into long-term cost control. SOLAR TODO uses this market context to position solutions across residential hybrid systems, commercial carports, and utility-scale ground-mount projects.

Global capacity and additions trend

Global solar PV grew from about 760 GW in 2020 to 1,419 GW in 2023, and most 2024-2026 forecasts point to continued acceleration driven by China, Europe, the United States, India, and the Middle East.

| Year | Estimated Global PV Capacity | Annual Additions | Market Signal |

|---|---|---|---|

| 2020 | ~760 GW | ~140 GW | Recovery and policy-driven growth |

| 2021 | ~942 GW | ~182 GW | Strong utility and rooftop demand |

| 2022 | ~1,185 GW | ~243 GW | Supply chain stress but record builds |

| 2023 | 1,419 GW | 345.5 GW | Historic annual installation record |

| 2024e | ~1.8 TW | ~380-450 GW | Module price compression accelerates demand |

| 2025e | ~2.0 TW | ~450-550 GW | Storage coupling rises |

| 2026e | ~2.2-2.4 TW | ~500-650 GW | PV becomes default new-build power in many markets |

According to BloombergNEF (2024), global solar installations could surpass 600 GW in 2025 under high-case assumptions. According to Wood Mackenzie (2024), utility-scale solar remains one of the most competitive new-build resources across major power markets even after accounting for interconnection and curtailment risks.

Cost Trends, Technology Shifts, and Performance Benchmarks

Solar PV in 2026 is defined by module efficiencies of 22%-24.5%, utility-scale LCOE around $0.029-$0.049/kWh, and battery-backed hybrid systems that increasingly optimize self-consumption and resilience rather than exports alone.

According to IRENA (2024), the global weighted-average LCOE of newly commissioned utility-scale solar PV in 2023 was about $0.044/kWh, down dramatically from 2010 levels. Fraunhofer ISE (2024) reports that utility-scale solar in favorable regions can remain among the lowest-cost generation options, while commercial rooftop economics depend more heavily on retail tariffs, self-consumption ratio, and financing terms. For project managers, this means the cheapest module is not always the cheapest project.

N-type TOPCon has moved into the mainstream because it improves efficiency, lowers degradation, and performs better in high-temperature conditions than many legacy PERC products. According to NREL (2024), system yield still depends heavily on irradiance, temperature coefficient, shading, DC/AC ratio, and inverter clipping management. Buyers should therefore evaluate total energy yield per square meter and per dollar, not nameplate wattage alone.

Technology comparison for 2026 procurement

By 2026, N-type TOPCon and bifacial modules dominate many tenders because they combine 22.5%-24.5% efficiency, lower first-year degradation, and better long-term energy retention than older mainstream products.

| Technology | Typical Module Efficiency | Typical Use Case | Relative Capex | 25-30 Year Yield Outlook |

|---|---|---|---|---|

| P-type PERC | 20%-22% | Price-sensitive retrofit or legacy supply | Low | Moderate |

| N-type TOPCon | 22.5%-24.5% | Commercial rooftop, carport, C&I hybrid | Low-Mid | Strong |

| HJT | 23%-25% | Premium rooftop, high-temperature sites | Mid-High | Very strong |

| Bifacial + Tracker | 22%+ front-side equivalent | Utility-scale ground mount | Mid | Highest site-adjusted yield |

According to IEC 61215-1:2021 and IEC 61730-1:2023, module qualification and safety compliance remain foundational for bankability. According to BloombergNEF (2024), bankable supplier selection is increasingly important in an oversupplied market where low prices can mask execution and warranty risk.

Product benchmarks relevant to B2B buyers

Commercial and utility buyers should benchmark solutions by annual yield, backup capability, and site utilization, not only by upfront $/W pricing.

| Product Example | Core Specification | Annual Generation / Backup | Typical B2B Value |

|---|---|---|---|

| 20kW+50kWh Residential Solar+Storage | 20 kWp PV + 50 kWh LFP + hybrid inverter | 28-36 MWh/year; 3-8 kW critical loads for 6-16 hours | High self-consumption and outage resilience |

| 50kW Factory Solar Carport | 50 kWp TOPCon carport | 75-90 MWh/year | Parking monetization and daytime bill reduction |

| 1MW Pastoral-Solar Ground Mount | 1,000 kWp bifacial tracker | ~2,050 MWh/year | Dual land use and low LCOE utility output |

These benchmarks show why SOLAR TODO addresses multiple procurement profiles. A factory may value 20-30 covered parking bays and EV readiness, while a developer may prioritize sub-$0.03/kWh potential in a 1 MW tracker project. A residential compound in weak-grid regions may instead prioritize 50 kWh of LFP storage and diesel displacement.

Regional Breakdown: Capacity, Tariffs, and Growth Hotspots

Asia-Pacific leads global PV deployment with more than half of annual additions, while Europe, North America, the Middle East/Africa, and Latin America each offer distinct tariff, policy, and irradiance-driven investment cases.

Regional strategy matters because the same 1 MW project can produce 1,300 MWh/year in a cooler lower-irradiance market or more than 2,000 MWh/year in a high-sun tracker market. According to the IEA (2024), China remains the largest single market by annual installations, while Europe continues to expand distributed and utility-scale solar to reduce fuel imports. According to IRENA (2024), emerging markets in MENA, Sub-Saharan Africa, and Latin America are also improving competitiveness as solar displaces diesel and expensive grid supply.

| Region | 2025-2026 Market Position | Typical Yield Range | Typical Commercial Tariff Context | Key Buyer Consideration |

|---|---|---|---|---|

| Asia-Pacific | Largest global installation base | 1,300-1,800 kWh/kWp/year | $0.08-$0.16/kWh | Scale, supply access, land constraints |

| Europe | Fast policy-led deployment | 1,000-1,500 kWh/kWp/year | $0.12-$0.30/kWh | Self-consumption, grid congestion |

| North America | Strong IRA-driven pipeline | 1,200-1,700 kWh/kWp/year | $0.10-$0.20/kWh | Interconnection and domestic content |

| Middle East/Africa | Highest irradiation in many markets | 1,700-2,200 kWh/kWp/year | $0.08-$0.25/kWh or diesel offset | Utility tenders, weak-grid resilience |

| Latin America | Expanding C&I and utility demand | 1,400-2,000 kWh/kWp/year | $0.09-$0.22/kWh | Currency risk and distributed generation rules |

Regional investment implications

Europe often delivers strong rooftop and carport economics because retail power prices can exceed $0.20/kWh, making self-consumption highly valuable. North America benefits from policy support and large utility pipelines, but interconnection queues can delay revenue realization by 12-36 months. The Middle East and Africa can produce some of the world’s lowest solar costs, especially where solar replaces diesel generation above $0.20-$0.35/kWh equivalent.

Latin America remains attractive for C&I solar because industrial tariffs are often volatile and many sites have strong irradiance. Asia-Pacific remains the manufacturing and deployment center, but local competition can compress EPC margins. For exporters such as SOLAR TODO, regional success depends on tailoring technology, financing, and delivery terms to local grid and tariff structures.

EPC Investment Analysis and Pricing Structure

A bankable solar PV project in 2026 typically combines $0.03-$0.05/kWh generation economics, 4-8 year payback in strong C&I cases, and a pricing structure that clearly separates supply-only, delivered, and turnkey EPC scope.

For B2B buyers, EPC means Engineering, Procurement, and Construction delivered as one integrated package. That usually includes system design, equipment sourcing, structural and electrical engineering, logistics coordination, installation, testing, commissioning, and performance documentation. In larger projects, it may also include grid studies, civil works, SCADA integration, training, and O&M handover.

SOLAR TODO generally works through an inquiry-to-offline-quotation model rather than an online marketplace. This is important because project pricing depends on site conditions, mounting type, grid requirements, and shipping destination. For large projects above $1,000K, financing support may be available subject to project profile and credit review.

Three-tier pricing structure

A practical B2B procurement model separates product value from logistics and construction risk so buyers can compare offers on a like-for-like basis.

| Pricing Tier | What It Includes | Typical Buyer Profile | Cost Impact vs FOB |

|---|---|---|---|

| FOB Supply | Modules, inverters, structures, core BOS | EPCs with local installation teams | Baseline |

| CIF Delivered | FOB + ocean freight + insurance to destination port | Importers and distributors | +5%-12% |

| EPC Turnkey | CIF-equivalent equipment + installation, commissioning, engineering, documentation | End users, developers, industrial owners | +10%-20% |

Volume pricing guidance for standardized procurement can follow this structure:

- 50+ units or equivalent project packages: about 5% discount

- 100+ units or equivalent project packages: about 10% discount

- 250+ units or equivalent project packages: about 15% discount

Typical payment terms are:

- 30% T/T deposit and 70% against B/L

- Or 100% L/C at sight

For quotation support, buyers can contact cinn@solartodo.com. This structure helps procurement teams compare landed cost, installation responsibility, and warranty boundaries before contract signature.

ROI and payback by application

Project economics vary most by tariff, irradiance, and self-consumption ratio, not by module price alone.

| Application | System Size | Annual Output | Savings Assumption | Typical Payback |

|---|---|---|---|---|

| Residential hybrid villa | 20 kWp + 50 kWh | 28-36 MWh/year | 50%-85% purchased power reduction | 6-10 years |

| Factory solar carport | 50 kWp | 75-90 MWh/year | $7,500-$16,200/year at $0.10-$0.18/kWh | 4-7 years |

| Utility/agri-PV ground mount | 1 MWp | ~2,050 MWh/year | PPA or self-use dependent | 5-9 years |

According to NREL PVWatts methodology, yield variation of 10%-20% between sites is common even for similar system sizes. That is why SOLAR TODO and other serious suppliers should model irradiance, temperature, shading, and export assumptions before issuing investment-grade proposals.

2030-2035 Outlook and Long-Term Market Scenarios

By 2035, global solar PV could exceed 5-7 TW under mainstream scenarios, with storage coupling, grid digitalization, and higher-efficiency modules reshaping both utility and behind-the-meter project design.

The next decade will not be driven by module cost declines alone. It will be driven by the integration challenge: storage, flexible demand, EV charging, grid-forming inverters, and digital energy management. According to the IEA World Energy Outlook (2024), electricity demand growth from cooling, transport, data centers, and industry will require much faster deployment of low-cost renewables. According to BNEF Global Energy Transition Investment (2024), clean energy investment is already measured in the trillions of dollars annually, with solar attracting a major share.

Wood Mackenzie notes that project bottlenecks are increasingly found in transmission, permitting, and interconnection rather than panel supply. Fraunhofer ISE states, "Photovoltaics is now one of the cheapest forms of electricity generation." For decision-makers, this means future competitiveness will depend on execution quality and grid integration more than on whether solar itself is economical.

Scenario view: 2027-2030 and 2030-2040

From 2027 to 2030, the market is likely to see more hybrid PPAs, more mandatory storage attachment in constrained grids, and greater use of AI-based forecasting. From 2030 to 2040, tandem cells, advanced inverters, and long-duration storage could materially improve dispatch value, especially in evening peak markets.

Likely technology evolution includes:

- Module efficiency moving from 22%-24.5% mainstream toward 25%+ premium products

- Wider use of bifacial trackers in utility plants where land and wind conditions permit

- More DC-coupled storage in C&I and utility projects

- Greater emphasis on recycling, traceability, and embodied-carbon reporting

- More smart infrastructure integration, including EV charging, telecom loads, and agricultural monitoring

For buyers planning 2026 procurements, the best strategy is to secure bankable technology now while designing assets that can integrate storage, EV charging, and digital controls later. That is especially relevant for SOLAR TODO customers in Latin America, the Middle East, Africa, and Southeast Asia, where grid quality and tariff structures vary widely.

FAQ

Solar PV buyers in 2026 need concise answers on cost, technology, EPC scope, and risk because project returns can vary by 10%-20% based on design and contract structure alone.

Q: What is driving global solar PV growth in 2026? A: The main drivers are lower module prices, energy security concerns, and electrification demand. Global installed capacity is moving above roughly 2.2 TW by 2026, while annual additions in many forecasts reach 500-650 GW, making solar one of the fastest-scaling energy technologies in history.

Q: How low are solar PV generation costs in 2026? A: Utility-scale solar commonly falls in the $0.029-$0.049/kWh range in strong-resource markets. According to IRENA, the 2023 global weighted-average LCOE for utility-scale solar was about $0.044/kWh, and competitive projects in high-irradiance regions can still perform below that benchmark.

Q: Which module technology is best for new B2B projects? A: N-type TOPCon is the most practical mainstream choice for many 2026 projects because it delivers about 22.5%-24.5% efficiency with strong temperature performance and lower degradation. HJT can be attractive for premium applications, while bifacial tracker systems remain strong for utility-scale ground-mount sites.

Q: How should I compare rooftop, carport, and ground-mount solar? A: Compare them by yield, structural complexity, and site value. Rooftops minimize land use, carports add parking and EV integration, and ground-mount systems usually offer the lowest LCOE at scale; for example, a 50 kWp carport can generate about 75-90 MWh/year, while a 1 MW tracker plant can reach roughly 2,050 MWh/year.

Q: What payback period should commercial buyers expect? A: Many commercial and industrial systems achieve payback in about 4-7 years when tariffs are $0.10-$0.18/kWh and self-consumption is high. Payback extends if export compensation is weak, but storage or load shifting can recover value in markets with time-of-use pricing.

Q: What does EPC turnkey delivery include? A: EPC turnkey delivery usually includes engineering, procurement, installation, testing, commissioning, and handover documentation. In larger projects it may also include civil works, grid studies, SCADA, operator training, and O&M setup, which reduces interface risk compared with supply-only contracts.

Q: How does SOLAR TODO price solar PV projects? A: SOLAR TODO typically quotes through three layers: FOB Supply, CIF Delivered, and EPC Turnkey. Standard guidance is about 5% discount for 50+ units, 10% for 100+, and 15% for 250+, with payment terms of 30% T/T plus 70% against B/L or 100% L/C at sight.

Q: When does battery storage make economic sense with solar PV? A: Storage makes sense when grid outages are frequent, export tariffs are low, or peak pricing is high. A 50 kWh LFP battery, for example, can support 3-8 kW of critical load for around 6-16 hours, making it valuable for resilience and self-consumption optimization.

Q: What certifications should procurement teams require? A: At minimum, require IEC 61215 and IEC 61730 for module qualification and safety, plus IEEE 1547 or local equivalent for interconnection where applicable. These standards support bankability, insurance acceptance, and long-term performance assurance over a 25-30 year operating life.

Q: What are the biggest risks in the 2026 solar market? A: The biggest risks are interconnection delays, supplier bankability, logistics volatility, and poor yield modeling. In an oversupplied module market, very low prices can hide warranty or delivery risk, so buyers should evaluate technical compliance, financial strength, and EPC execution history together.

References

- IRENA (2024): Renewable Capacity Statistics 2024, reporting 1,419 GW of global solar capacity in 2023 and 345.5 GW annual additions.

- IEA (2024): Renewables 2024 and World Energy Outlook 2024, outlining solar PV growth trajectories and electrification demand trends.

- NREL (2024): PVWatts Calculator methodology and performance modeling guidance for solar yield estimation.

- Fraunhofer ISE (2024): Photovoltaics Report, covering global deployment, technology trends, and cost benchmarks.

- BloombergNEF (2024): Global solar installation outlook and Tier 1 manufacturer bankability assessments.

- Wood Mackenzie (2024): Global solar market and utility-scale project pipeline analysis, including interconnection and deployment constraints.

- IEC 61215-1:2021 (2021): Terrestrial photovoltaic modules design qualification and type approval requirements.

- IEC 61730-1:2023 (2023): Photovoltaic module safety qualification requirements for construction and testing.

Conclusion

Global solar PV in 2026 combines 2.2+ TW of installed capacity, sub-$0.05/kWh utility economics, and a credible path to 5-7 TW by 2035, making it a core power procurement strategy rather than an optional sustainability measure.

The bottom line is that buyers who combine bankable technology, accurate yield modeling, and clear EPC scope can secure 4-8 year paybacks today while building assets ready for storage, EV charging, and smart infrastructure integration through 2035.

About SOLARTODO

SOLARTODO is a global integrated solution provider specializing in solar power generation systems, energy-storage products, smart street-lighting and solar street-lighting, intelligent security & IoT linkage systems, power transmission towers, telecom communication towers, and smart-agriculture solutions for worldwide B2B customers.

About the Author

SOLAR TODO

Solar Energy & Infrastructure Expert Team

SOLAR TODO is a professional supplier of solar energy, energy storage, smart lighting, smart agriculture, security systems, communication towers, and power tower equipment.

Our technical team has over 15 years of experience in renewable energy and infrastructure, providing high-quality products and solutions to B2B customers worldwide.

Expertise: PV system design, energy storage optimization, smart lighting integration, smart agriculture monitoring, security system integration, communication and power tower supply.

Cite This Article

SOLAR TODO. (2026). Global Solar PV Market Report 2026. SOLAR TODO. Retrieved from https://solartodo.com/knowledge/global-solar-pv-market-report-2026-capacity-cost-trends-2035-outlook

@article{solartodo_global_solar_pv_market_report_2026_capacity_cost_trends_2035_outlook,

title = {Global Solar PV Market Report 2026},

author = {SOLAR TODO},

journal = {SOLAR TODO Knowledge Base},

year = {2026},

url = {https://solartodo.com/knowledge/global-solar-pv-market-report-2026-capacity-cost-trends-2035-outlook},

note = {Accessed: 2026-04-21}

}Published: April 19, 2026 | Available at: https://solartodo.com/knowledge/global-solar-pv-market-report-2026-capacity-cost-trends-2035-outlook

Subscribe to Our Newsletter

Get the latest solar energy news and insights delivered to your inbox.

View All Articles